Which is the best Savings Account? [Solved]

Probably the most debated topic among final-year university gatherings as we begin our adulthood and pursue the golden dream of passive income. Among such conversations, we often find someone pitching one of these 3 accounts - OCBC 360, UOB One and DBS Multiplier. I thought I knew which account was best for me, but somehow I always ended up leaving these conversations with a different one in mind.

Honestly, these saving accounts are quite different from one another. With the way they structured their interests computation, OCBC 360 being highly complex and UOB One being a no-brainer, I wouldn’t be surprised you’re confused too! If you haven’t had the chance to read up more about their interest structure, here are their summaries from their pages:

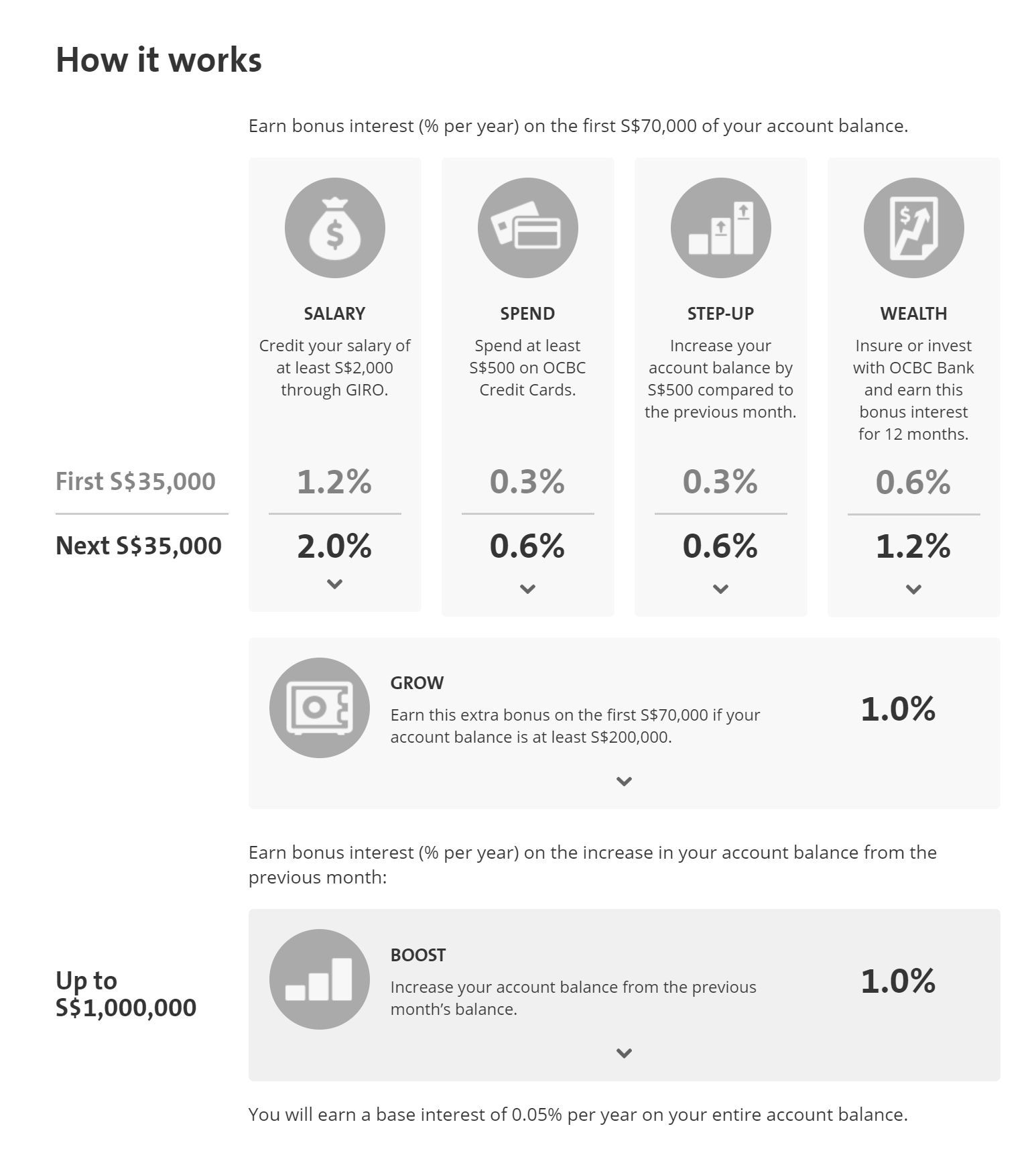

OCBC 360 Interest Structure — Most Complex

https://www.ocbc.com/personal-banking/accounts/360-account.html

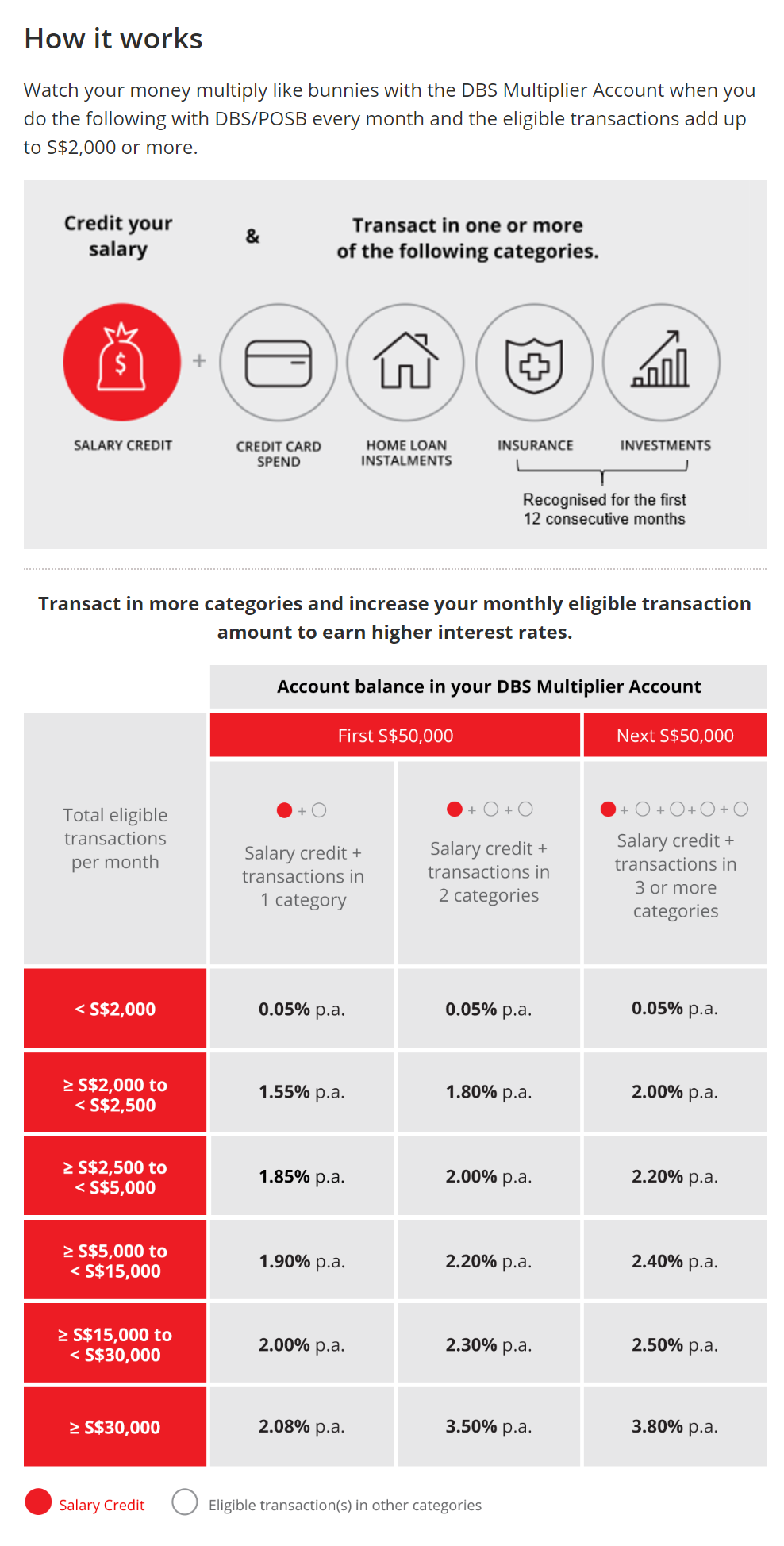

DBS Multiplier Interest Structure — Still Acceptable

https://dbs.com.sg/personal/deposits/bank-earn/multiplier

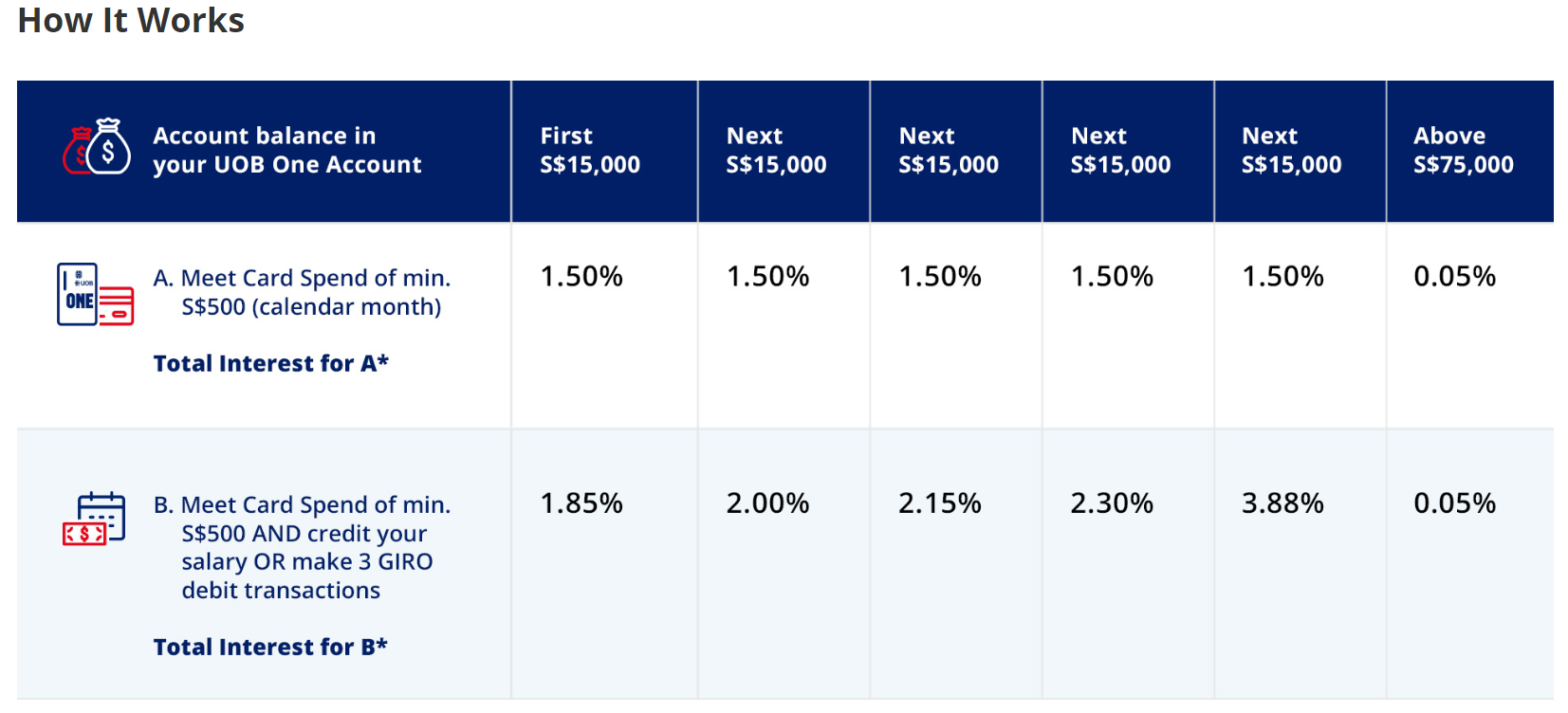

UOB Interest Structure — Least Complex

https://www.uob.com.sg/personal/save/chequeing/one-account.page

A simple hack

Personally, my initial choice was to create a DBS Multiplier account given that I did not have much savings for UOB One to be effective and OCBC 360 is just too complicated. However, after making some effort to crunch the numbers, I realized OCBC 360 would have given me the best interests.

With this conversation surfacing again in my recent gathering, I knew it was time to solve this once and for all. With numbers. Given each individual has their own spending habits, salary and saving patterns, what works best for me might not work for them. Hence, I created a Savings Account Calculator to help determine which is the best savings account given an individual’s circumstances.

Here’s how it works:

Let numbers do the talking 😊

Can you make it simpler?

Photo by Drew Coffman on Unsplash

One of my friends, whom I first shared the calculator with, said:

“I’m too lazy to fill up the calculator. Can you summarise your findings?”

Despite his laziness, I knew exactly where his pain is coming from. There are way too many articles and people making general statements such as:

“If you’re saving for big purchases, this is better for you” “If you want simplicity, just use DBS multiplier”

That leads to even more questions, how big is a big purchase? $1,000? $5,000? $100,000? Simplicity? What constitutes simplicity?

Therefore, I wanted to provide him a quantitative summary. I ran a couple of simulations *(shown next section) *and eventually managed to summarise the whole thing into 2 simple rules.

And they are…

Rule 1 — If you spend less than $500 on your credit card, go with DBS Multiplier. Otherwise, go to Rule 2. Rule 2 — If your account balance is less than $70,000, go with OCBC 360. Otherwise, go with UOB One. Bonus Rule — If you plan to invest with them for their bonus interest, always go with OCBC 360.

*Note: Not advisable, I believe that there are plenty of ways to earn this bonus interests. Also, please do your own due diligence to ensure that the bonus interests outweigh the fees and risks of those investments.

That’s all for my answer to “Which is the best Savings account?”. I hope this helped you decide a savings accounts in one way or another. For a more specific answer, do give Savings Account Calculator a try. Don’t be *lazy *like my friend. If you’re interested in how I derived the rules and what are the assumptions behind the calculator, read on!

The Simulations

As we have 5 variables (‘account balance’, ‘salary’, ‘credit card expense’, ‘savings’, ‘investment amount’) in play, I’ve decided to focus mainly on ‘account balance’, ‘salary’ and ‘credit card expense’ while keeping the others constant. For simplicity sake, salary here refers to net CPF (different from Savings Account Calculator). In this case, ‘savings’ is kept at 20% of salary and ‘investment amount’ is be kept at $0. The simulations are run in a 1-year time period, which means interests are compounded 12 times.

Credit Card Expense vs Salary

Account balance will be varied at 3 levels: $0, $50,000 and $100,000. Credit card expense is varied from $0 to $1,500 at $50 intervals and Salary is varied from $2000 to $10,000 at $100 intervals.

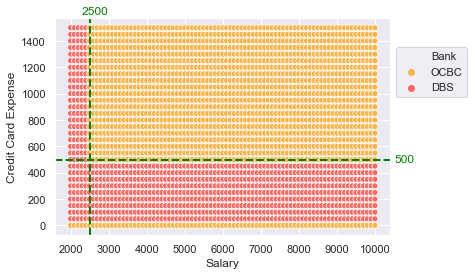

Account Balance: $0

A pretty clear cut answer when credit card expense goes above $500. Spend bonus from OCBC becomes the deciding factor. If your salary is below $2,500, DBS provides a stronger interest of 1.55% against OCBC’s salary and spend bonus (1.50% total).

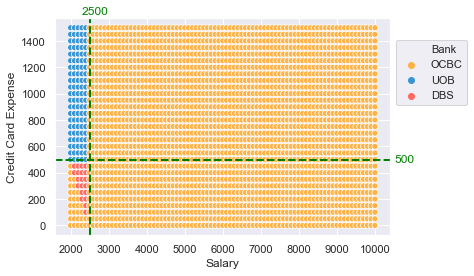

Account Balance: $50,000

OCBC dominates the chart as DBS has a cap on $50,000 mark. Unless you activate 3 categories, in which case we do not consider, beyond $50,000 you’ll only get 0.05% for them. Whereas, UOB lacks behind due to its simplistic structure.

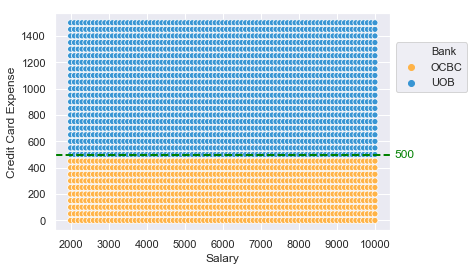

Account Balance: $100,000

As UOB has a higher cap of $75,000 compared to OCBC of $70,000, simply meeting the minimum spending of $500 to qualify for interest is sufficient for UOB to prevail.

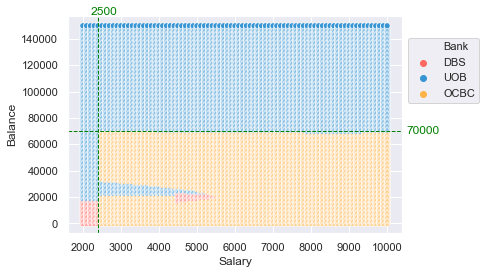

Account Balance vs Salary

Account balance is varied from $0 to $150,000 at $1000 intervals and Salary is varied from $2000 to $10,000 at $100 intervals. Card card expense is kept constant at $500.

Similarly, above an account balance of $70,000, UOB will provide better returns due to OCBC $70,000 cap. A bloody dagger is observed with an account balance of $20,000 to $30,000 with DBS being the tip of it. This is due to the juicy OCBC’s boost interest of 1% which is applied to savings (increment of the account balance each month), slowly eating away UOB. Not too sure about the ‘blood’ though.

With Investment

I’ve repeated all the simulations with investment at different amounts, all of which indicates OCBC giving the best interests. Some might argue that DBS factors in investment into the tier level, however, it seems that the investment amount must be substantial enough to tip the scale towards DBS.

Assumptions for Savings Account Calculator

You’re probably wondering if the calculator takes into account tiered interest in DBS? Or even growth bonus in OCBC? And I can imagine so many other similar questions. Thus, here’s a concise explanation of what goes behind the calculator.

- Monthly Salary — Salary before CPF. It deducts 20% automatically as CPF in its own calculation. If you’re non-Singaporean, put 1.25*salary instead.

- Credit Card Expense — Spending on your credit card. This will be used to factor if you quality for UOB, DBS and OCBC bonus interest. All of them minimally require $500 in spending.

- Monthly Savings — The increase in your account balance every month. This usually means the amount that is left from your salary.

- Planning to Invest — Lets you indicate if you plan to invest with OCBC or DBS or Both in which you fulfill their investment criteria to earn their bonus interest. Refer to their website for their criteria.

- Monthly Investment — Only used for DBS calculation whereby your investment amount is added to transactions in order to determine tier.

- For OCBC 360, the calculator factors all the bonus interest if you qualify (salary, spend, step-up, wealth, grow, boost) and base interest of 0.05%. Base interest is credited end of the year on the overall balance.

- For DBS Multiplier, the calculator factors salary credit, bonus interest tiers for both 1 and 2 categories (credit card + invest) and base interest of 0.05% beyond the 50k cap.

- For UOB One, the calculator factors the 2 tiers of interests if you qualify for the $500 credit card expenditure, salary credit. It also applies the base interest of 0.05% beyond the 75k cap. Also, when calculating interest earned from your balance, $500 is deducted to estimate your daily average balance for the month.

- All bonus interests are credited monthly, therefore, they are divided by 12 when used in calculations.

- Cashbacks and rewards from credit card expenses are not taken into consideration.

If there are any other queries about the calculations or a better savings account to recommend, feel free to share it with me. As for the code, I have uploaded them onto my GitHub account. Also, this is based on my own personal understanding of the 3 accounts, do highlight to me if you find any errors in my code. It’ll be greatly appreciated! Cheers!